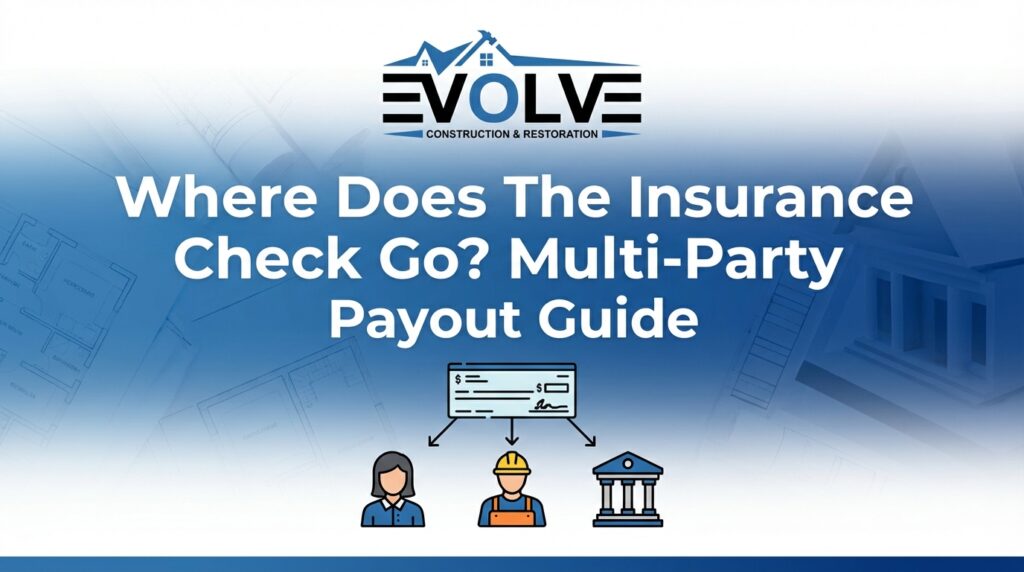

Receiving an insurance settlement check after a major storm or property loss should be a moment of relief. However, for many homeowners, that relief quickly turns into confusion or even frustration when they look at the “Pay to the Order Of” line. Instead of just seeing their own name, they find a string of names including their mortgage lender, a public adjuster, and perhaps a restoration contractor. This leads to the urgent question: Where does the insurance check go?

The complexity of multi-party payouts is one of the most common sources of consumer complaints in the restoration industry. Many homeowners feel that their funds are being “held hostage” by third parties like public adjusters or banks. At Evolve Construction, we believe transparency is the key to a stress-free rebuild. This guide will demystify the escrow process, explain why these legal safeguards exist, and provide a clear roadmap for getting your funds released so your project can stay on track.

Featured Snippet Answer: An insurance check goes to the parties who have a legal “insurable interest” in the property. This typically includes the homeowner, the mortgage lender, and any hired public adjuster. Because the home is collateral for your loan, the lender must ensure funds are used for repairs. Money is often held in a restricted escrow account and released in installments (draws) as work progresses.

1. Understanding Multi-Party Insurance Checks: Why Your Lender is Listed

The primary reason your mortgage company appears on your insurance check is a legal concept known as “insurable interest.” When you signed your mortgage agreement, you agreed to a “mortgage clause” that protects the lender’s investment. Because the bank technically owns a significant portion of your home’s value until the loan is paid off, they have a right to ensure that insurance proceeds are used to restore the property to its original condition, rather than being spent elsewhere.

The Lender as a Loss Payee

Your homeowner’s insurance policy lists your mortgage company as a “loss payee.” This designation mandates that the insurance company include the lender on any payout related to structural damage. If the insurance company were to pay you directly and you failed to repair the roof or the foundation, the bank’s collateral (your home) would decrease in value, putting their loan at risk. By being named on the check, the lender gains oversight of the restoration process.

The Role of Public Adjusters (NICA, Bulldog, etc.)

If you hired a public adjuster, such as NICA or Bulldog Adjusters, to represent you, their name will also appear on the check. This is standard industry practice because you likely signed a “Letter of Protection” or a contract granting them a percentage of the settlement for their services. Their inclusion ensures they are paid for the professional negotiation they provided. While it may feel like more red tape, their presence on the check is a legal requirement based on the contract you signed with them.

Protecting the Homeowner

While it feels like the bank is interfering, this process also protects you from unscrupulous contractors. Since the bank won’t release the final “draw” until they verify the work is done via an inspection, it ensures the contractor follows through on their promises. At Evolve Construction, we often help our clients navigate this paperwork to ensure the transition from “check in hand” to “work on the roof” is as seamless as possible.

2. The Payee Line: The Legal Difference Between ‘And’ vs. ‘Or’

One of the most critical details on your insurance check is a single word: “And” or “Or.” This determines exactly how much effort you will have to put into depositing the funds. Most insurance checks are written as “Homeowner AND Mortgage Company AND Public Adjuster.” This phrasing creates a cumulative legal requirement, meaning every single party listed must endorse (sign) the back of the check before it can be processed by a bank.

The Restrictive Nature of ‘And’

When the word “And” is used, the check is considered a joint-payee instrument. You cannot simply sign it and deposit it into your personal savings account. If you attempt to do so, your bank will likely reject the deposit or place a long-term hold on the funds. The “And” serves as a safeguard to ensure that no one party can abscond with the funds without the knowledge and consent of the others involved in the property’s protection.

The Rare ‘Or’ Scenario

In rare instances, a check might be made out to “Homeowner OR Mortgage Company.” In this scenario, any one of the listed parties could theoretically endorse and deposit the check. However, insurance companies almost never use “Or” for structural damage claims because it bypasses the mortgage company’s oversight. If you see “Or” on a check for personal property or Additional Living Expenses (ALE), it is much easier to manage, as you can deposit it directly.

Managing Endorsements Correctly

To handle an “And” check, you must first get your signature on it, then the public adjuster’s signature (if applicable), and finally send it to the mortgage lender. We recommend using trackable mail (like FedEx or UPS) whenever sending a multi-thousand-dollar check to a lender’s loss draft department. Losing a multi-party check in the mail can add weeks of delay to your restoration project while the insurance company goes through the process of voiding and reissuing the payment.

3. The Loss Draft Process: How Your Mortgage Company Handles Your Funds

Once you send the signed check to your lender, it enters the “Loss Draft” department. This is a specialized division within a mortgage company that does nothing but manage insurance claim funds. They do not simply sign the check and send it back to you. Instead, they deposit the funds into a restricted escrow account—a temporary holding tank for your repair money.

What is a Loss Draft?

The term “loss draft” refers to the check itself, but the process refers to the managed release of those funds. The lender’s goal is to ensure the money is disbursed in a way that matches the progress of the repairs. This protects the lender from a situation where a homeowner receives $50,000, spends it on a new car, and leaves the house with a leaking roof that eventually leads to mold and structural failure.

Trust Accounts and Legal Compliance

For public adjusters and contractors, placing funds into trust or escrow accounts is not just about organization—it is about legal compliance. Many states have strict regulations requiring that insurance proceeds for property repairs be held in fiduciary accounts. This prevents the commingling of personal funds with project funds. When you see your funds sitting in an escrow account, it is a sign that the process is working according to the law to ensure your project is fully funded from start to finish.

Digital Loss Draft Portals

Many modern lenders now offer digital portals for managing loss drafts. Instead of calling and waiting on hold, you can upload your contractor’s estimate, W-9, and photos of the progress directly to their website. This has significantly sped up the time it takes to get funds released. If your lender offers a portal, Evolve Construction recommends using it, as it provides a clear paper trail and faster communication than traditional mail and phone calls.

4. Claim Size Thresholds: When the Lender Hands Over the Check vs. Holds It in Escrow

The level of oversight your mortgage company exerts depends heavily on the size of the check. Lenders have specific “thresholds” that determine whether they will simply endorse the check and give it back to you or whether they will keep it in escrow and require progress inspections. Understanding these thresholds can help you set realistic expectations for your project timeline.

Small Claims (Low Oversight)

For smaller claims—typically those under $10,000 or $15,000 (though some lenders go up to $40,000)—the mortgage company may choose to “monitor-free” the claim. In these cases, you send them the check, they endorse it, and they mail it back to you within a few days. They trust you to manage the repairs without them verifying every nail and shingle. This is common for minor storm damage restoration or small gutter repairs.

Large Claims (High Oversight)

When a claim exceeds the lender’s threshold (often $20,000 or more), they will almost certainly hold the funds in escrow. At this stage, they become a project manager of sorts. They will release the money in “draws” and will require an inspection after each phase of the work is completed. This is the standard procedure for major residential roofing replacements or full-scale interior remodeling following water damage.

Regional and Lender Differences

It is important to note that these thresholds are not universal. A local credit union might have different rules than a national bank like Wells Fargo or Chase. Additionally, if your loan is backed by the FHA or VA, there may be specific federal guidelines that the lender must follow regarding the disbursement of insurance funds. Always check your lender’s specific “Loss Draft Package” for their exact numbers.

5. Step-by-Step: Getting Your Insurance Check Endorsed and Deposited

Navigating the endorsement process requires a specific order of operations. Skipping a step or sending the check to the wrong department can lead to the check being returned or lost. Follow this step-by-step guide to move the money from the insurance company to your repair project as quickly as possible.

- Verify the Payees: Check the front of the check. Are all names spelled correctly? If your public adjuster’s name is misspelled, the bank may reject it later.

- Obtain Adjuster Endorsement: If a public adjuster is listed, they must sign the back first. Often, they will sign it and hand it to you, or they may have you sign it and then they take it to the lender.

- Contact the Loss Draft Department: Do not just mail the check to your local bank branch. Call your mortgage servicer and ask for the “Loss Draft Department” or “Insurance Claims Department.” Ask for the specific mailing address and the list of required documents.

- Mail via Trackable Service: Send the endorsed check along with a copy of the insurance adjuster’s estimate and your contractor’s signed contract. Use FedEx or UPS so you have proof of delivery.

- Confirm Receipt: Wait 48 hours after delivery and call the lender to ensure the check has been received and the escrow account has been opened.

Common Pitfalls in the Endorsement Phase

One common mistake is forgetting to sign the check yourself before sending it to the lender. If you send an unsigned check, the lender cannot deposit it into escrow, and they will have to mail it back to you, wasting at least a week. Another pitfall is failing to include the “Claim Number” or “Loan Number” on the back of the check and on all accompanying paperwork. Mortgage companies handle thousands of claims; without these numbers, your check could sit in a processing pile for days.

6. The Disbursement Schedule: How ‘Draws’ and Progress Inspections Work

If your funds are held in escrow, they will be released in a series of payments called “draws.” This system is designed to provide the contractor with working capital while ensuring the homeowner and lender are protected against incomplete work. At Evolve Construction, we are very familiar with this rhythm and work closely with lenders to provide the necessary documentation for each draw.

Initial Draw (Deposit)

25% – 33%

Signed contract, W-9, and insurance estimate.

Progress Draw

33% – 50%

Verification of materials on-site or 50% completion.

Final Draw

Remaining Balance

Passing inspection and Certificate of Completion.

The Initial Draw and Mobilization

The first check released by the lender is usually intended for “mobilization.” This covers the cost of ordering materials (like shingles, siding, or windows) and permits. Lenders generally release this as soon as they have the contract and have verified the contractor is licensed and insured. If you are working with a reputable company like Evolve, we handle the document submission to get these funds moving.

Progress Inspections

For the second and third draws, the lender will often send a third-party inspector to your home. This person is not there to judge the quality of the craftsmanship (though they might notice obvious issues); they are simply there to verify that the work described in the insurance estimate is actually happening. They will take photos of the progress and send a report back to the bank. Once the report is processed, the next check is cut.

The Final Release

The final draw is released only after the project is 100% complete. You will likely be asked to sign a “Certificate of Completion” or a “Satisfaction Affidavit.” Once the lender receives this document and their inspector confirms the project is finished, they release the final funds. This final check is often made out to both you and the contractor to ensure the bill is paid in full.

7. Documentation Checklist: What You Must Provide to the Loss Draft Department

To avoid delays, you must be proactive in providing documentation. Lenders are notoriously bureaucratic; if a single document is missing or unsigned, the entire process can grind to a halt. We recommend creating a digital folder of these documents as soon as your claim is approved.

- The Insurance Adjuster’s Full Report: The lender needs to see the line-item breakdown of what the insurance company is paying for.

- Contractor’s Signed Contract: A formal agreement between you and the repair company showing the total cost.

- Contractor’s W-9 Form: The lender needs this for tax reporting purposes before they can pay a third party.

- Contractor’s License and General Liability Insurance: Proof that the company is qualified and covered to do the work.

- Conditional Lien Waivers: Documents from the contractor stating they won’t place a lien on your home once they receive the specific draw amount.

- Letter of Authorization: A form that allows your contractor or public adjuster to speak directly with the lender on your behalf.

Why the W-9 is Crucial

Many homeowners are surprised that the bank asks for the contractor’s W-9. Since the bank is technically the one issuing the payment from the escrow account, the IRS views it as a payment made by the bank. Without a W-9 on file, the bank’s software may literally prevent them from cutting a check. Ensure your contractor provides a current, signed W-9 early in the process.

8. Exceptions to the Rule: Personal Property and Additional Living Expenses (ALE)

Not all insurance money has to go through the lender. It is important to differentiate between structural repair funds and other types of payouts. If your insurance company sends you a single check that combines all these categories, you may want to ask them to split the payments to avoid having your “grocery money” stuck in a mortgage escrow account.

Additional Living Expenses (ALE)

ALE funds are intended to cover the extra costs of living (like hotel stays or dining out) because your home is uninhabitable. Since these funds have nothing to do with the structural value of the home, the mortgage company has no legal right to them. ALE checks should be made out to you alone. If the lender’s name is on an ALE check, contact your insurance adjuster immediately to have it reissued.

Personal Property (Contents)

Similarly, payouts for your furniture, electronics, and clothing (personal property) are usually for you alone. The bank’s mortgage covers the land and the structure, not your flat-screen TV. Most insurance companies will issue separate checks for contents, but if they don’t, you’ll have to go through the endorsement process. However, you can often request that the lender release 100% of the contents portion of a joint check immediately.

9. Troubleshooting Delays: What to Do if the Lender Withholds Funds Unreasonably

Sometimes, despite your best efforts, the lender may be slow to release funds. This can put your contractor in a difficult position and stall your repairs. If you feel the lender is withholding funds unreasonably, there are several steps you can take to escalate the situation.

Escalate to a Supervisor

The person answering the phone in the Loss Draft department is often a low-level clerk following a script. If your project is 50% done but they refuse to release the second draw, ask to speak to a “Loss Draft Supervisor” or an “Escrow Manager.” Explain the situation clearly: “The contractor has materials on site and a crew ready, but we need the mobilization funds to continue.”

Involve Your State’s Department of Insurance

While the Department of Insurance primarily regulates insurance companies, they can often provide guidance if a mortgage company is obstructing a claim. Additionally, many states have laws (like the Prompt Payment Act) that require timely processing of funds. Mentioning that you are aware of these regulations can sometimes “grease the wheels” of a slow bank department.

Leverage Your Contractor

At Evolve Construction, we deal with loss draft departments daily. We know the lingo they want to hear and the specific forms they require. If you are facing a delay, let us help. We can provide the necessary affidavits or inspection photos that might be the missing piece of the puzzle for the bank.

10. Special Situations: Multiple Lienholders, Mortgage Default, and Surplus Funds

Real-world property ownership isn’t always straightforward. There are several “outlier” scenarios that can significantly change how insurance checks are handled. Being aware of these can prevent major surprises down the road.

Multiple Lienholders (Second Mortgages and HELOCs)

If you have a second mortgage or a Home Equity Line of Credit (HELOC), that lender may also be listed on the check. This means you now have four parties who need to sign: you, the primary lender, the secondary lender, and the public adjuster. This creates a “daisy chain” of mailings. Usually, the primary lender (with the largest interest) will be the one to manage the escrow account, but you must still get the second lender to endorse the check first.

Mortgage Default and Foreclosure

If you are currently behind on your mortgage payments, the bank’s behavior will change. Instead of releasing the funds for repairs, they may have the legal right to apply the insurance proceeds directly to your loan balance. This is a complex legal area, and if you are in default, you should consult with an attorney or a specialized insurance claims assistant to understand your rights and ensure your home is actually repaired.

Surplus Funds

What happens if you complete all the repairs for $45,000, but the insurance check was for $50,000? Once the lender’s inspector verifies that the home is fully restored to its pre-loss condition, any remaining money in the escrow account belongs to you. The bank cannot keep the surplus to pay down your principal unless you specifically authorize them to do so.

11. Conclusion: Tips for Streamlining Your Multi-Party Payout

Understanding where the insurance check goes is the first step in taking control of your property restoration. While the multi-party payout process involves significant red tape, it is ultimately a system designed to ensure the integrity of your home and the legality of the financial transaction. By staying organized, using trackable mail, and communicating frequently with both your lender and your contractor, you can minimize delays and focus on what really matters: getting your home back to normal.

To streamline your process, always ask for a “Loss Draft Packet” from your lender as soon as you file a claim. Keep copies of everything you send, and don’t be afraid to ask your restoration team for help. At Evolve Construction, we stand with our clients through every phase of the project—from the first inspection to the final signature on the escrow release. Together, we can navigate the complexities of insurance payouts and build a better tomorrow for your property.

Ready to Get Started?

Our honest, friendly, and reputable professionals help homeowners and businesses maximize the value of their property and stand together with them to rebuild for a better tomorrow, especially after challenging storm events.